Creditas Financial Results Q1-2026

Accelerating sustainable growth by balancing gross profit generation with disciplined investments in customer acquisition, automation and our AI platform

São Paulo, 07th May 2026

Business Context

Key Highlights – Q1 2026

Portfolio

Record Origination at R$1.1bn (+29.2% YoY and +2.1% QoQ). We sustained robust momentum across all lending business units, with Auto and Home Equity posting all-time-high quarterly volumes and e-Consignado consistently regaining pace through the period while keeping conservative risk-reward balance.

Portfolio reached R$7.6bn or +22.4% YoY (+6.4% QoQ), tracking within our annual growth target despite the revised interest rate environment in Brazil with SELIC remaining higher for longer.

Financials

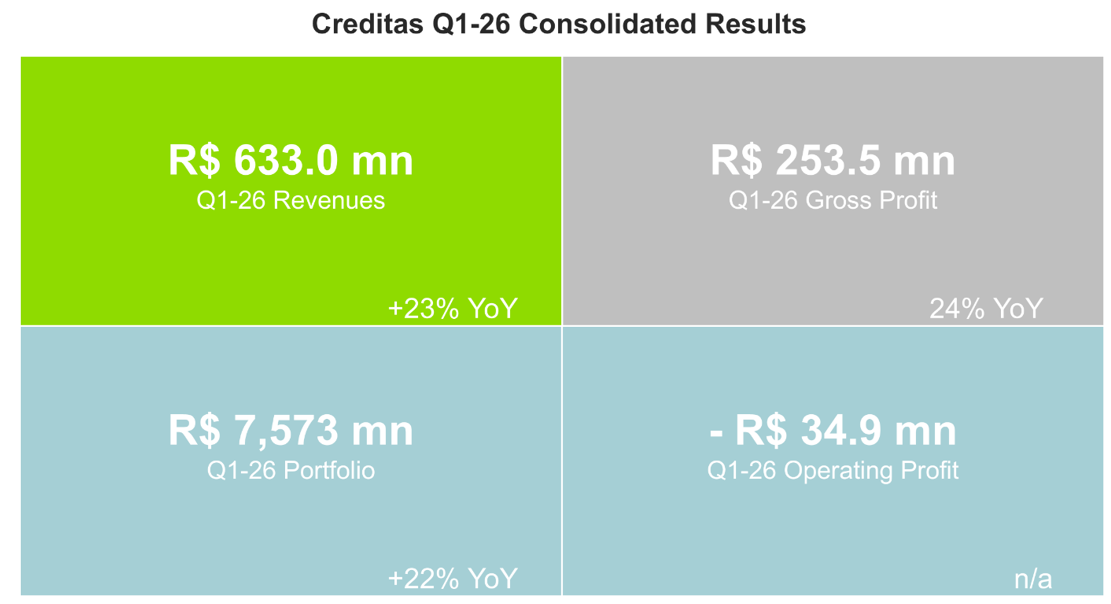

Revenues grew to R$633.0mn (+23.1% YoY and +8.6% QoQ) driven by portfolio scale and consistent pricing execution.

Record quarterly Gross Profit at R$253.5mn (+24.1% YoY and +20.0% QoQ), representing a 40.0% Gross Profit Margin. After several quarters of accelerated origination growth where front-loaded IFRS provisioning temporarily compressed results, margins are now stabilizing and converging toward our target cohort-level profitability of 40-45%, confirming the strength of our unit economics.

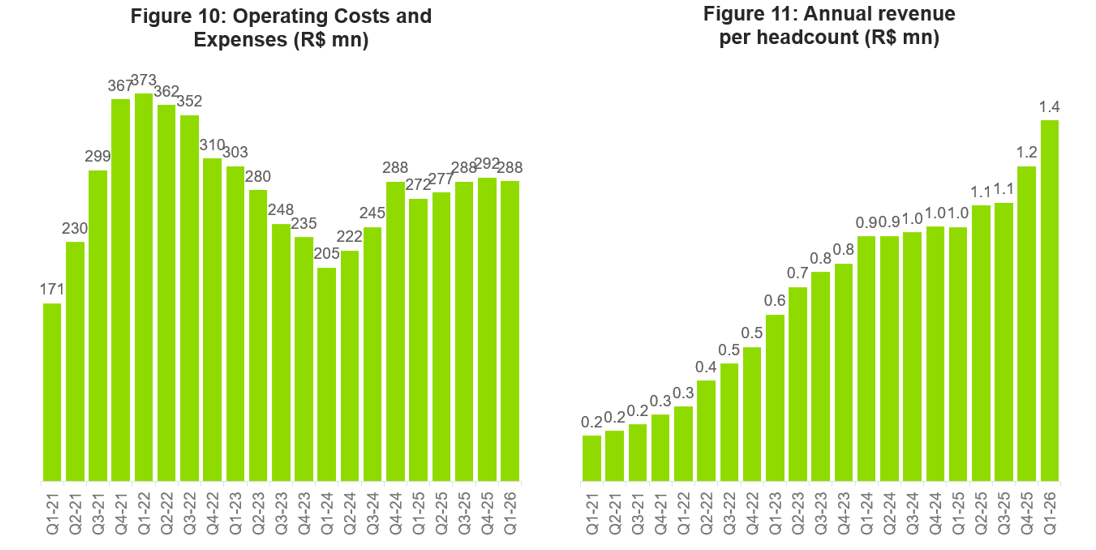

Operating Costs and Expenses improved to R$288.4mn (-1.3% QoQ), reflecting our disciplined approach to growth investments and continued scale gain in corporate expenses.

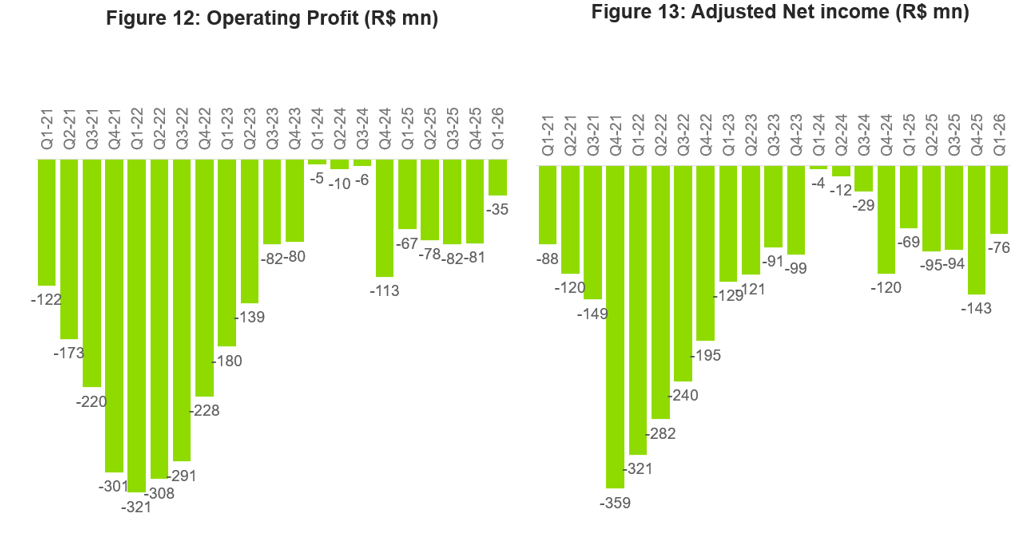

Operating loss narrowed to R$34.9mn (vs. R$80.9mn in Q4-25), approximately one-tenth of the level in Q1-22 despite higher origination levels, underscoring our vastly improved efficiency. We remain laser-focused on maintaining a cash-neutral operation, while optimizing investments in highly profitable growth.

Operations

Portfolio momentum continued to accelerate broadly across our business units in Q1-26, with every vertical contributing to record-level origination. This performance was underpinned by the successful validation of our latest Auto Equity pricing model and the disciplined expansion in e-Consignado, where operational processes continue to improve and we maintain a selective approach to risk and pricing. By combining technological advancements with continuous funnel automation, we achieved structural CAC reduction that allowed us to scale origination to record levels while continuing to improve cohort-level profitability.

Significant traction in process automation drove productivity metrics to record highs as we strategically accelerated AI developments across customer experience, collections, operational processes, and coding. We are currently deploying AI agents to handle our end-to-end experience in early-stage collections and to streamline origination for high-end client profiles, enabling transactions to be completed within minutes rather than hours or days. In software development, AI-led pull requests are compressing our product cycle from three weeks to four days. Together, these advancements are delivering tangible value across the company, as clearly perceived in the rise of our productivity from R$1.1mn to R$1.4mn in annualized revenues per headcount over the last 6 months.

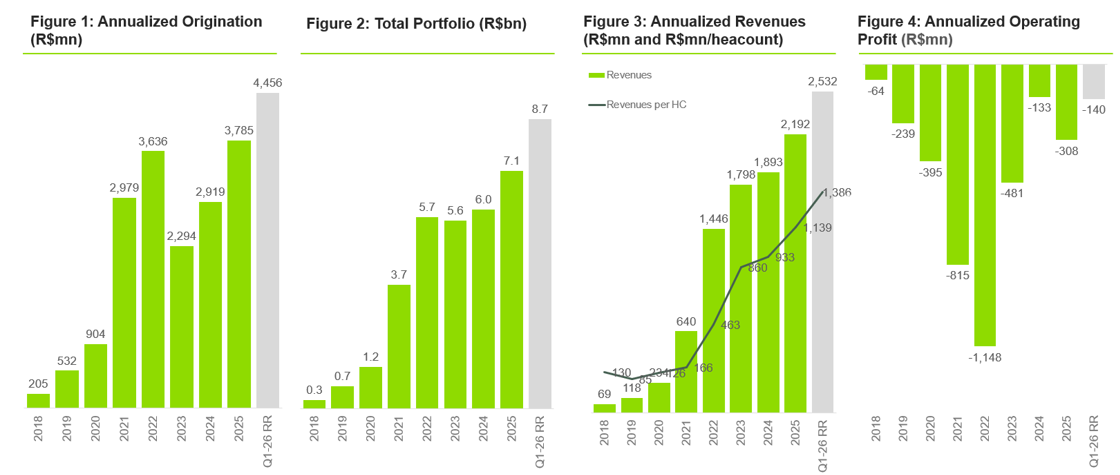

The results achieved in Q1-26 highlight our continued progress in balancing scale with operational efficiency. When annualizing our first-quarter performance, the figures reflect a notable transition in the company’s financial position including more than R$4.4bn in annual origination to bring portfolio to R$8.7bn (+22% YoY), with annualized revenues above R$2.5bn and operating loss run rate less than half of last year. While these annualized metrics already provide a solid baseline, the ongoing maturation of our efficiency initiatives and AI-driven optimizations is expected to further enhance performance, positioning the company to enter a new phase by year end that combines strong growth and profitability.

First Quarter Financial & Operating Results

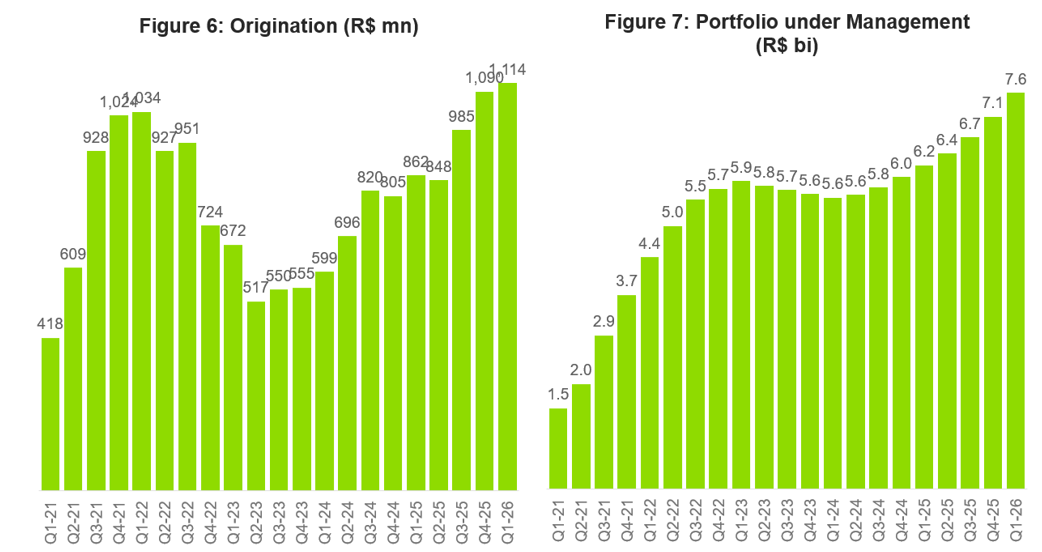

In Q1-2026, we maintained our rigorous focus on profitable growth, delivering record results across all verticals. Origination increased 29.2% YoY and our Portfolio grew 22.4% YoY (see Figure 6 and Figure 7). This performance represents an all-time high, marking a significant milestone: we are now driving record expansion while maintaining highly profitable cohorts and optimized operational productivity. This approach represents a structural evolution from the volume-led growth of the 2020-2021 period, prioritizing high-quality earnings as we resume scaling, even though the long-term nature of our loans delays the recognition of this profitability in IFRS results.

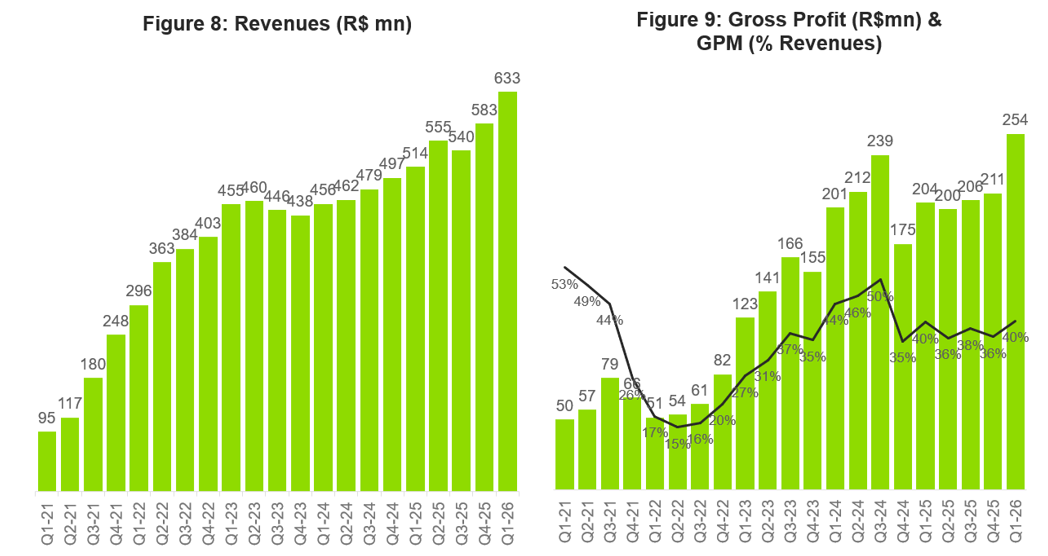

The continued expansion of our Portfolio supported Revenue growth to R$633.0mn (+23.1% YoY and +8.6% QoQ) (see Figure 8), continuing the consistent scaling trajectory of recent quarters. The standout of the quarter, however, was Gross Profit, which reached a record R$253.5mn (+24.1% YoY and +20.0% QoQ) at a 40% Gross Profit margin, reflecting a stabilizing origination pace and the resulting normalization of associated provisions (see Figure 9). While quarterly fluctuations may persist depending on origination mix and growth pace, the structural trajectory of our unit economics remains firmly on track toward our 40-45% goal. Reported margins continue to converge toward this target as two primary factors normalize: (i) interest rates, which positively impact margins as CDI converges with long-term rates and aligns with the swap rate embedded in our portfolio pricing; and (ii) IFRS provisioning front-loading, which eases as the origination level stabilizes. Crucially, underlying cohort profitability remains well above our 40% target, providing the foundation to sustain our long-term strategy.

Operating Costs and Expenses (see Figure 10) totaled R$288.4mn, declining 1.3% QoQ. This stable-to-declining cost trajectory — achieved while origination grew +29.2% YoY — is highly relevant to our platform’s operational leverage and reflects a deliberate discipline in scaling efficiently. Customer Acquisition Costs (CAC) as a percentage of origination continued to compress meaningfully across our main verticals, evidencing our ability to scale growth without a proportional increase in expenses. Our focus on building an AI-first architecture is yielding record productivity, with revenue per employee reaching a new high of R$1.4mn (see Figure 11). AI is being embedded across every layer of our platform — from collections, where autonomous agents handle ~90% of interactions in early-stage delinquency at near-zero marginal cost and outperforming human-agent benchmarks, to software development, where AI agents increasingly execute end-to-end pull requests. These advancements have driven a 14x growth in revenue per employee since Q1-19, with productivity accelerating by an additional 40% over the last six months alone as a direct result of deploying AI agents across operational and product workflows. Unlike market practices that often outsource core functions such as technology, collections, or sales, we internalize these operations to capture superior scale gains. Consistent with our conservative accounting framework, we recognize all acquisition and technology costs upfront, while loan and insurance margins accrue over time.

Our focus remains on reinvesting portfolio profit to drive growth, a strategy anchored by strong unit economics and short payback periods. While the combined effect of accelerated growth and the inverted interest rate curve impacts short-term reported profitability, we are prioritizing net present value built on superior IRRs to generate strong future cash flows. This discipline is clearly reflected in our Q1-26 results, where operating loss narrowed significantly to R$34.9 million (vs. R$80.9mn in Q4-25), driven by strong gross profit expansion and disciplined cost management (see Figure 12). Net loss for the quarter totaled R$75.9mn (see Figure 13). Importantly, we maintained a neutral cash flow position, which enables us to fund our growth internally without the need for external capital – a key pillar of our long-term strategy. This quarter’s performance underscores the strength of our discipline in portfolio expansion and an accelerated trajectory toward operational profitability on an IFRS basis.

Business Unit Performance

Auto Equity

Auto Equity delivered a record quarter with 18.7% YoY portfolio growth, following the successful validation of the latest pricing model implementation and continued efficiency gains across the product’s acquisition funnels. This performance reinforces the product’s position as our flagship and underscores the significant operational leverage still to be unlocked. The strength of the product’s unit economics provides a solid foundation for further efficiency gains as we build momentum through 2026.

Home Equity

Home Equity also delivered its largest origination quarter ever, with 33.8% YoY portfolio growth consolidating its position among the market leaders. This performance was driven by continuous acquisition funnel evolution and a fundamentally AI-driven underwriting back-office: 90% of first-line credit analyses are automated, legal review and contract generation are 100% AI-assisted, and 60% of signature validations require no human intervention. This structural advantage significantly reduces processing times, allowing us to scale both direct-to-consumer and affiliate networks with superior efficiency.

Private Employees Payroll Loans

Building on increased visibility into e-Consignado unit economics and the normalization of operational processes, we are gradually broadening our customer coverage. In Q1-26 we reached an average coverage of 12.5% of the addressable private employee market. Having already adapted to the new regulatory interest rate caps, we are now refining our client targeting to capture the right profiles without compromising our growth trajectory or margin expectations.

Auto Finance

After gaining confidence in the product’s unit economics and operational flow, we continue to accelerate growth in 2026, reaching 40.2% YoY portfolio expansion. Building on the underwriting playbook developed and validated in Home Equity, we are now extending agent-based automation to the Auto Finance credit workflow. This initiative aims to shorten time-to-close and scale decisioning capacity without proportional headcount additions, positioning Auto Finance for a profitable and balanced expansion.

Insurance

We continue focused on refining the insurance user experience and consolidating Creditas as the largest independent online broker in Brazil. We are committed to unlocking the product’s full potential through multiple avenues, including the integration of AI assistants to boost consultant productivity, viewing Insurance as a strategic component that will add significant scale to our platform over the coming years.

Business Outlook

Creditas is in a new growth phase, supported by a foundation of high client recurrence, strong credit performance, and clear product-market fit across all core offerings. We are increasingly evolving into an AI-first platform, embedding automation into every layer of our operations, making it the structural engine of our productivity. This transformation is already reshaping how we acquire customers, manage credit, and run our back office, positioning us for an annual growth target of 25%+, while maintaining portfolio profitability and targeting a return to operational break-even in the near term.

Subscribe for

updates

Receive all our news in your email